At 1st Florida Lending we offer Florida & California home

purchases and refinances plus non-owner-occupied investor

and commercial property financing in AL, AZ, CA, GA, FL, IL,

IA, KS, KY, LA, MN, MT, ND, OK, PA, SC, SD, TX, and WV

Florida’s Top-Rated Direct Mortgage Lender

Offering 48+ Loan Programs

A+ BBB Rated I 4.8 Google Reviews

Trusted Direct Lender with Decades of Experience

Servicing Florida and California for Purchases

and Refinancing Primary and Second Homes Offering

Investment and Commercial Properties Nationwide

CARLOS MATOS - CEO & FOUNDER

A FEW HIGHLIGHTS

48+ PROGRAMS with LOW RATES

DIRECT LENDER - NOT BROKERS

WE LIKE CHALLENGING LOANS

SAME DAY PRE-APPROVAL LETTERS

TRUSTED LENDER FROM FL TO CA

CALL OR TEXT US AT 407-300-2558

1st Florida Lending Corp., a registered Mortgage Lender

Orlando servicing only the State of Florida, offering over

48 loans programs including Conventional Loans, Non-

Conforming Loans, FHA Loans, VA Loans, USDA Loan,

Self-Employed Loans, Bank Statement Loans, No-Doc

Loans, Reverse Mortgage Loans, ITIN Loans, Rental

Investment Loans, to name a few and specializing in

Bank Statement Loans or “stated loans” requiring no Tax

Return verification and much more. * No broker or

lender fees are for FHA,VA, USDA and Conventional

loan types

Main Office: 2151 Consulate Dr. * Suite 8 * Orlando,

FL., 32837 * Telephone * (800)856-7097 * (800) 655-

1345 * (407) 300-2558 * Fax (877) 401-9955

* Disclaimer: All Loan programs, rates and terms can

change without notice and are subject to credit and

underwriting approval. Loan charts highlight min/max

constraints, assumptions & random scenarios only. We will

always work hard to approve your loan but there are no

guarantees of any kind expressed or implied that any loan

we be approved. Licensed in Florida Only. When Banks

Say No ! We Say YES ! ® is a registered trademark owned

by 1st Florida Lending Corp. Florida lender license #

MLD106.

© 2007 - 2026 1st Florida Lending Corp. - All rights reserved

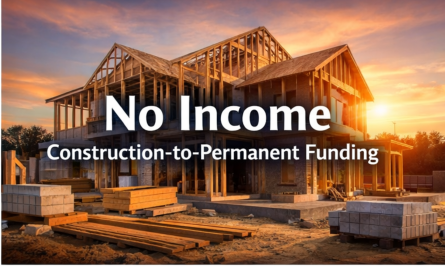

TWO PROGRAM OPTIONS

We Offer Two Construction-to-Permanent

Funding Programs

PROGRAM 1: Conventional, VA and Self-

Employed Construction-to-Permanent

Funding utilizing both traditional and self-

employed financing for borrowers with

documented income, strong credit, and a

stable financial profile.

PROGRAM 2: No Doc Construction-to-

Perm Funding utilizing alternative

financing for investors, and borrowers

with non-traditional income who prefer

not to provide tax returns or traditional

income documentation.

One-Time Close Construction Financing

allows you to build and finance your

primary residence, second home, or

investment property with a single loan

and one closing. This streamlined

approach combines both the construction

phase and the permanent mortgage into

one seamless transaction, eliminating the

need for multiple loan applications and

duplicate closing costs.

By consolidating the process into one

loan, borrowers benefit from reduced

paperwork, faster approvals, and a more

efficient path from groundbreaking to

move-in. During construction, funds are

disbursed in stages to your builder, and

once the project is complete, the loan

automatically converts into long-term

financing without the need for a second

closing or re-qualification.

The result is a simplified, cost-effective

financing solution that provides greater

convenience, improved cash flow

management, and peace of mind

throughout the entire building process.

How It Works

•

Apply once for both construction and

permanent financing.

•

Close once: pay just one set of closing

costs.

•

Draw funds: as your project

progresses (foundation, framing,

finishing).

•

Convert automatically to a traditional

mortgage: (15- or 30-year term) when

construction ends.

•

Enjoy fixed rates: and predictable

payments on your completed home.

•

Typical construction period: up to 12

months (it varies by project).

Why Choose 1st Florida Lending?

•

Competitive rates: on both

construction and permanent financing

•

Flexible draw schedule: tailored to

your build timeline

•

Expert guidance: through every phase

form land purchase to construction

draws, inspection, and permanent

conversion

•

Interest-only payments: during the

build phase to manage cash flow

•

Local expertise: Deep knowledge of

Florida construction costs, permitting,

and market trends

READY TO START? Choose a

program below, click on image

for more program details, the

approval process and request a

quote.

We offer over 48 loan programs in every

county in the State of Florida as follows;

Alachua County,Baker County,Bay

County,Bradford County,Brevard County,Broward

County,Calhoun County,Charlotte County,Citrus

County,Clay County,Collier County,Columbia

County,DeSoto County,Dixie County,Duval

County,Escambia County,Flagler County,Franklin

County,Gadsden County,Gilchrist County,Glades

County,Gulf County,Hamilton County,Hardee

County,Hendry County,Hernando

County,Highlands County,Hillsborough

County,Holmes County,Indian River

County,Jackson County,Jefferson

County,Lafayette County,Lake County,Lee

County,Leon County,Levy County,Liberty

County,Madison County,Manatee County,Marion

County,Martin County,Miami-Dade

County,Monroe County,Nassau County,Okaloosa

County,Okeechobee County,Orange

County,Osceola County,Palm Beach

County,Pasco County,Pinellas County,Polk

County,Putnam County,Santa Rosa

County,Sarasota County,Seminole County,St.

Johns County,St. Lucie County,Sumter

County,Suwannee County,Taylor County,Union

County,Volusia County,Wakulla County,Walton

County,Washington County

- FHA LOANS - 4 Programs

- BANK STATEMENT LOAN

- SELF-EMPLOYED SECOND

- CONVENTION HOME LOANS

- PROFIT AND LOSS LOANS

- ASSET DEPLETION LOANS

- JUMBO LOANS

- INVESTMENT PROPERTY LOANS

- NO DOC FUNDING (7 Programs)

- VACANT LAND LOANS

- COMMERCIAL PROPERTY LOANS

- VA HOME LOANS

- USDA HOME LOANS

- ABOUT US

- CONSTRUCTION LOANS

- FOREIGN NATIONAL LOANS

- ITIN LOAN PRGOGRAM

- CONTACT US